Types of Costs by Behavior

Cost behavior refers to the relationship between total costs and activity level. Based on behavior, costs are categorized as either fixed, variable or mixed. Fixed costs are constant regardless of activity level, variable costs change proportionately with output and mixed costs are a combination of both.

Fixed Costs

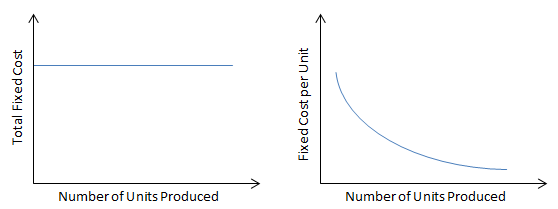

Fixed costs are those which do not change with the level of activity within the relevant range. These costs will be incurred even if no units are produced. For example rent expense, straight-line depreciation expense, etc.

Fixed cost per unit decreases with increase in production. Following example explains this fact:

| Total Fixed Cost | $30,000 | $30,000 | $30,000 |

| ÷ Units Produced | 5,000 | 10,000 | 15,000 |

| Fixed Cost per Unit | $6.00 | $3.00 | $2.00 |

Variable Costs

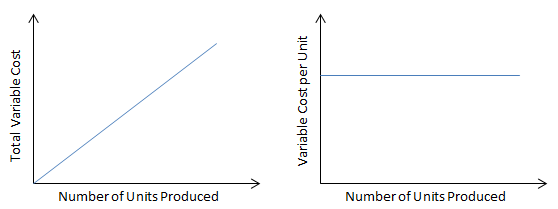

Variable costs change in direct proportion to the level of production. This means that total variable cost increase when more units are produced and decreases when less units are produced. Average variable cost i.e. variable cost per unit is constant . For example

| Total Variable Cost | $10,000 | $20,000 | $30,000 |

| ÷ Units Produced | 5,000 | 10,000 | 15,000 |

| Variable Cost per Unit | $2.00 | $2.00 | $2.00 |

Mixed Costs

Mixed costs or semi-variable costs have properties of both fixed and variable costs due to the presence of both variable and fixed components in them. An example of mixed cost is telephone expense because it usually consists of a fixed component such as line rent and fixed subscription charges as well as variable cost charged per minute cost. Another mixed cost example is delivery cost which has a fixed component of depreciation cost of trucks and a variable component of fuel expense.

Since mixed cost figures are not useful in their raw form, therefore they are split into their fixed and variable components by using cost behavior analysis techniques such as High-Low Method, Scatter Graph Method and Regression Analysis.

The following table shows a comparison of different costs classifications based on behavior:

| Category | Fixed Costs | Variable Costs | Mixed Costs |

|---|---|---|---|

| Total cost | Constant | Changes proportionately with output | Change with output but not proportionately |

| Cost per unit | Decreases with increase in output | Constant | Decreases with increase in output but less than the decrease in fixed cost per unit |

| Examples | Plant depreciation, property taxes | Fuel expense, wages, raw materials | Telecommunication costs, senior management salaries, transportation cost |

by Irfanullah Jan, ACCA and last modified on